Brazil: New Oil Drive Impacts

Oil-rich Brazil!

Despite his commitment to the environment, President

Lula wants to revive Brazil's oil industry for two reasons: 1) to increase

important federal revenues for his social programs, 2) to ensure Brazil's

energy security, recognizing that the energy transition will take time.

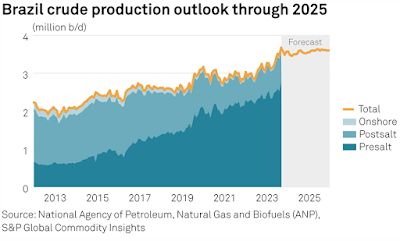

Brazil has become a major player in the oil market and

is expected to consolidate production at 4 million barrels per day. This is not

sudden. It is the product of decades of sustained oil policy, even under

Bolsonaro or Temer, of exploration and development that respects the plans of

Petrobras, its partners, and a stable legal framework. As production in the

pre-salt grows, Brazil is likely to use the time to explore opportunities to

diversify its export market beyond its traditional buyers. Brazil is also

taking advantage of the decline in Venezuelan, Mexican and Argentine oil due to

misguided policies and poor management. While looking for new markets, possibly

in regions such as Asia, Brazil understands the importance of maintaining solid

relations with its traditional buyers such as the United States. That is why

the United States is not concerned about Brazil's membership in OPEC+. This

dual approach ensures a balanced oil export strategy, serving established

markets while expanding into new ones to optimize its growing production

capacity.

What is operational?

In late December, Petrobras brought the Sepetiba FPSO on stream in the Mero pre-salt field in the Santos Basin, with another FPSO planned for the field later this year. The new unit will add an additional 180,000 b/d of oil and 424 mmscfd of gas capacity. In 2024, the Mero pre-salt field stands out as the main project responsible for boosting domestic production, in particular the start-up of the Sepetiba FPSO and the commissioning of the third Mero FPSO. After 2024, production growth will be driven by the installation of new FPSOs on assets already producing in the pre-salt, such as Búzios and Mero. In the next two years, production is expected to remain relatively stable as the planned FPSOs gradually come on stream.

What's next for Brazilian oil?

OPEC forecasts that Brazil will add about 120,000 b/d

in 2024, averaging 4.2 million b/d for the year, compared with 400,000 b/d of

additions and 4.1 million b/d in 2023. Crude oil growth is expected to come

mainly from the Mero, Búzios and, to a lesser extent, Tupi, Peregrino and Itapu

fields. In 2025, Petrobras plans to add five new pre-salt units in the Santos

and Campos basins. Between 2024 and 2028, the state-owned company will add

another six FPSOs in the giant Búzios field, bringing the company's total to

14. Petrobras has earmarked 73% of its planned capital expenditure for 2024-28

for exploration and production.

Brazil is always looking to expand its upstream

supply. On December 13, Brazil's oil,and gas agency, ANP, celebrated the fourth

cycle of its open acreage under concession regime and the second cycle of its

open acreage in production sharing (OAPS) regime. Of particular interest was

the Pelotas Basin. In this basin, 44 blocks out of a total of 192 exploration

blocks were awarded in the fourth cycle. Pelotas had not received any bids

since the sixth bidding round.

The government hopes that the geology of the Pelotas

Basin is similar to that of the Namibian Basin on the other side of the

Atlantic. The South American plate broke away from Africa during the Cretaceous

period. Several major oil discoveries have been made in Namibia in recent

years. The oil production potential of Brazil's Pelotas Basin remains

speculative until further exploration drilling and appraisal is completed.

Typically, the transition from discovery to development in such basins can take

8 to 10 years, indicating that this is a long-term prospect rather than a

short-term solution. Production has now gone through this period first.

Meanwhile, also in the second cycle of the OAPS regime, BP acquired the

Tupinamba block in the Santos Basin, but no bids were received for the

remaining four blocks.

The likelihood of additional bid rounds in 2024

depends on industry interest. Brazil's "standing offer" system, which

allows interested parties to nominate areas for exploration, provides a

flexible framework for initiating bid rounds based on market interest and

potential. Within this framework, Brazil's NOC has also earmarked 41.5% of its

2024-28 exploration budget for the Equatorial Margin, which covers the mouth of

the Amazon. Oil exploration is controversial in the region, but the government

says the geology could prove similar to that of Suriname and Guyana. The

state-owned company intends to test the region's oil potential by drilling at

least 16 wells and will continue to search.

Geopolitical implications

Brazil boasts annual production growth of nearly 20%

through December and has ambitions to become the fourth largest oil producer by

2030. Increasing domestic production is at the heart of Brazil's recent

admission to OPEC+. The pact recognizes the country's growing influence,

particularly as pre-salt oil increases, while the Brazilian government also

wants to build closer economic and political ties with the world's largest

exporters. OPEC+ membership would allow Brazil to forge closer ties with other MENA

regional powers, particularly Saudi Arabia, OPEC's most influential member.

Petrobras intends to make investments for development

in several countries, such as Venezuela (if Maduro fixes or optimizes its oil

industry), Colombia, Bolivia and Argentina, although the details and concrete

plans for these projects have yet to be determined. For now, a lot of good will has been

generated, but it remains to be seen how it will be translated into concrete

actions. It should be remembered that "Brazilians are good talkers",

although it is certain that as long as the PT remains in power, there will be

ample opportunities for investment. A conservative candidate who clashes with

the rest of the government would be another matter. The United States is not

concerned about this issue because the more production the better, and OPEC+ is

the one that always does the hard work necessary to maintain competitive prices

for American crude. In other words, OPEC+ is not so cruel with the price

because it is in the interest of a growing global economy and at the same time

helps maintain competitive prices for more expensive crudes like U.S. crude. It's a

win-win.

Comments

Post a Comment